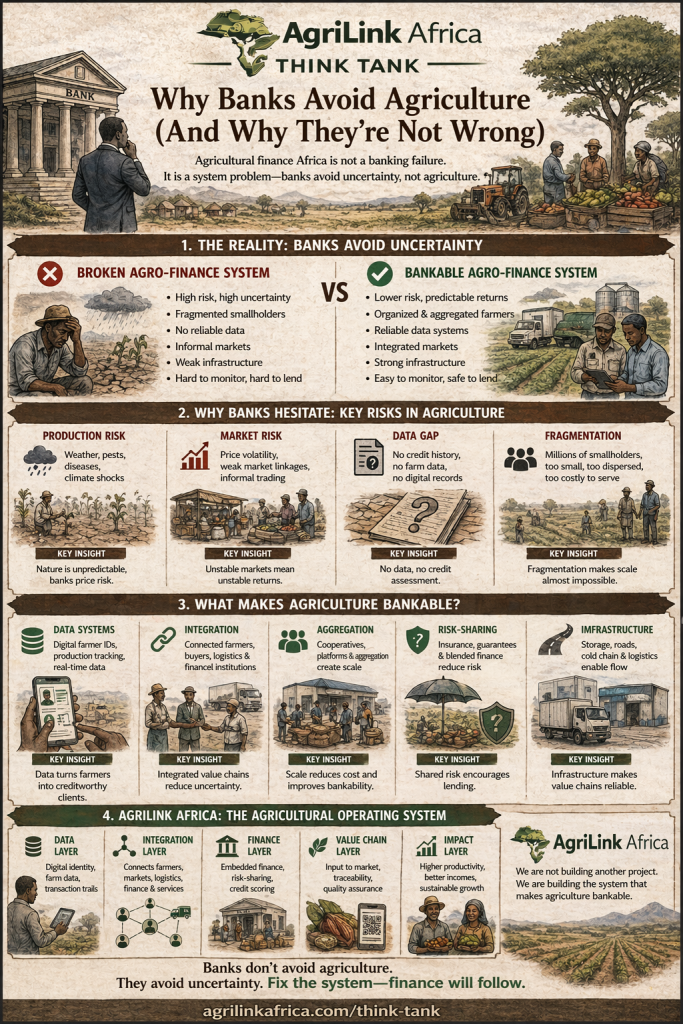

Agricultural finance Africa: a system problem, not a banking failure

Agricultural finance Africa remains one of the most debated challenges in the continent’s development agenda. Policymakers often frame the issue as a failure of banks—arguing that financial institutions are too risk-averse, too urban-focused, and disconnected from rural economies.

But this narrative is incomplete—and in many ways, misleading.

Banks are not irrational actors. They price risk. They allocate capital where systems are predictable, data is available, and returns are measurable. In much of Africa’s agricultural sector, these conditions simply do not exist.

This article argues a contrarian but necessary point: banks avoid agriculture not because they are wrong, but because the system is broken. The real issue lies in the structural foundations of agricultural finance Africa—namely:

- Lack of systems

- Lack of integration

- Lack of data infrastructure

Rather than forcing banks to change behavior, Africa must focus on building an agricultural operating system that makes the sector bankable by design.

The reality of agricultural finance Africa

Agriculture contributes significantly to GDP and employment across Africa, yet it receives disproportionately low levels of formal financing. According to the World Bank and FAO, 2021, less than 10% of total bank lending in many African countries goes to agriculture.

This gap is not accidental. It reflects deep structural constraints that shape how financial institutions assess risk.

Why banks hesitate: the risk perspective

From a banking standpoint, agriculture presents a unique combination of risks:

- Production risk

- Weather variability

- Pests and diseases

- Climate shocks

- Market risk

- Price volatility

- Weak market linkages

- Informal trading systems

- Operational risk

- Fragmented smallholder base

- Poor logistics and storage

- Limited aggregation

- Information risk

- Lack of credit history

- Absence of reliable farm-level data

- Informal land tenure systems

As highlighted by the International Fund for Agricultural Development (IFAD), these risks are compounded by weak rural financial infrastructure.

In short: banks are not avoiding agriculture—they are avoiding uncertainty.

The core issue: Lack of systems in agricultural finance Africa

The deeper problem in agricultural finance Africa is not risk alone—it is the absence of structured systems that reduce and manage that risk.

This aligns directly with the argument made in our previous analysis:

👉 Why Africa Needs Agricultural Operating Systems, Not More Projects

What does “lack of systems” mean?

It means agriculture in many African countries operates without:

- Standardized data collection

- Integrated value chain coordination

- Digitized transaction records

- Scalable aggregation mechanisms

Without these elements, agriculture remains invisible to formal finance.

Fragmentation: the invisible barrier to agricultural finance Africa

One of the most critical structural challenges is fragmentation.

The smallholder paradox

Africa’s agriculture is dominated by millions of smallholder farmers, each operating independently. While collectively significant, individually they are:

- Too small to finance

- Too dispersed to monitor

- Too informal to assess

This creates a paradox:

The sector is large, but its units are too small for banking systems to engage efficiently.

Why fragmentation scares banks

Banks rely on scale and standardization. Fragmentation leads to:

- High transaction costs

- Difficulty in loan monitoring

- Increased default risk perception

As discussed in:

👉 Why Agricultural Policies Collapse Between Capital Cities and Villages

The disconnect between policy design and field-level realities further deepens this fragmentation.

The data gap: Why agriculture is “unbankable” on paper

In modern finance, data is collateral.

In agriculture across Africa, data is either missing or unreliable.

What data is missing?

- Farm production records

- Yield histories

- Input usage

- Market transactions

- Credit repayment behavior

Without this data, banks cannot:

- Assess creditworthiness

- Price loans accurately

- Monitor performance

According to CGAP, digital financial services can significantly reduce this gap—but adoption remains limited.

Lack of integration: disconnected value chains

Agricultural value chains in Africa are often disjointed:

- Farmers produce without guaranteed buyers

- Traders operate informally

- Processors lack consistent supply

- Logistics are inefficient

This lack of integration increases uncertainty across the entire chain.

Why integration matters for finance

Banks prefer financing structured flows, not isolated actors.

For example, financing works better when:

- Farmers are linked to buyers (contract farming)

- Inputs are tracked and financed

- Outputs are aggregated and sold through formal channels

This is explored further in:

👉 Policy Alignment Failure: When Ministries Don’t Talk

Without integration, agriculture remains a high-risk, low-visibility sector.

Stop blaming banks: Fix the system instead

Blaming banks for avoiding agriculture is like blaming doctors for avoiding a disease without treatment protocols.

The solution is not to pressure banks—but to transform the underlying system.

Building an agricultural operating system for Africa

To unlock agricultural finance Africa, the continent must shift from project-based interventions to system-based transformation.

1. Build data systems for farmers

Digitization is the foundation of bankability.

Key actions:

- Create digital farmer IDs

- Track production and transaction data

- Use mobile platforms for data collection

Example:

Platforms like digital farmer registries and mobile-based extension systems can generate bankable data trails.

Related insight:

👉 Why Africa Needs Agricultural Operating Systems, Not More Projects

2. Digitize value chains

End-to-end digitization reduces uncertainty.

This includes:

- Input supply tracking

- Production monitoring

- Market transactions

- Payment systems

According to GSMA, mobile technology is already enabling digital agriculture solutions across Africa.

3. Use cooperatives and platforms to reduce fragmentation

Aggregation is essential.

Approaches:

- Strengthen farmer cooperatives

- Build digital marketplaces

- Create platform-based ecosystems

This transforms millions of small farmers into organized, financeable units.

4. Introduce risk-sharing models

Banks will lend when risks are shared.

Key instruments:

- Agricultural insurance

- Credit guarantees

- Blended finance mechanisms

The African Development Bank emphasizes risk-sharing as a key driver of agricultural lending.

5. Make agriculture bankable by design

Ultimately, the goal is not to convince banks—it is to change the structure of agriculture.

A bankable system has:

- Reliable data

- Predictable cash flows

- Integrated value chains

- Reduced transaction costs

When these conditions are met, finance follows naturally.

AgriLink Africa: Building the Agricultural Operating System Africa Needs

At AgriLink Africa, we recognize that the constraints in agricultural finance Africa are not isolated problems—they are symptoms of a missing system.

This is why we are not building another project.

We are building an Agricultural Operating System.

AgriLink Africa is designed as an integrated ecosystem that directly addresses the structural gaps outlined in this analysis:

What AgriLink Africa is solving

1. Lack of data infrastructure

- Digital farmer profiling and identity systems

- Real-time production and transaction tracking

- Creation of verifiable data trails for financial institutions

2. Lack of integration

- Connecting farmers, buyers, logistics providers, and financial institutions

- Enabling structured value chain coordination

- Bridging rural production with urban markets

3. Fragmentation of smallholder systems

- Aggregating farmers through digital platforms and cooperatives

- Creating scale where none previously existed

- Transforming informal actors into organized economic units

4. Financial exclusion in agriculture

- Embedding financial services within the platform

- Enabling risk-sharing models (insurance, guarantees, blended finance)

- Making agriculture bankable by design—not by force

From concept to system transformation

AgriLink Africa operationalizes the very shift this article calls for:

- From projects → systems

- From fragmentation → integration

- From invisibility → data-driven agriculture

- From high risk → structured, financeable ecosystems

This is not a theoretical framework.

It is a practical infrastructure layer for agricultural transformation in Africa.

As explored in our foundational thinking:

👉 Why Africa Needs Agricultural Operating Systems, Not More Projects

AgriLink Africa stands as a direct response to that gap—a platform designed to make agricultural finance Africa work at scale.

From projects to systems: A paradigm shift

For decades, agricultural development in Africa has relied on fragmented projects.

These projects:

- Are short-term

- Lack scalability

- Fail to build lasting infrastructure

As discussed in:

👉 Agricultural Operating Systems Africa: The Missing Infrastructure

The future lies in building systems, not implementing projects.

Policy implications for agricultural finance Africa

To unlock financing at scale, policymakers must:

1. Prioritize digital infrastructure

- National farmer registries

- Data-sharing frameworks

2. Align ministries and institutions

- Agriculture

- Finance

- ICT

3. Enable private sector platforms

- Encourage agri-tech ecosystems

- Support innovation

4. De-risk agriculture

- Subsidize insurance

- Provide guarantees

5. Shift from subsidies to systems

- Invest in infrastructure, not handouts

Conclusion: Banks are rational—systems must evolve

Agricultural finance Africa will not improve by forcing banks to lend into broken systems.

Banks are doing what they are designed to do: manage risk and allocate capital efficiently.

The responsibility lies elsewhere.

Africa must build:

- Data systems

- Integrated value chains

- Aggregation platforms

- Risk-sharing mechanisms

Only then will agriculture become visible, predictable, and bankable.

The future of agricultural finance Africa is not about changing banks.

It is about building the operating system that agriculture has always lacked.

A Call to Action: Building the Future Together

Transforming agricultural finance Africa requires more than ideas—it requires coordinated action across stakeholders.

We invite collaboration from:

- Policymakers – to align regulatory and institutional frameworks

- Financial institutions – to co-develop innovative financing models

- Development partners – to support system-level investments

- Agri-tech innovators – to integrate and scale solutions

- Farmer organizations and cooperatives – to drive grassroots adoption

AgriLink Africa is not just a platform.

It is a shared infrastructure for a new agricultural economy.

If Africa is to unlock the full potential of its agricultural sector, the path forward is clear:

Build systems. Integrate actors. Digitize value chains. Enable finance.

That is why we stand by our name—AgriLink Africa.

Because the future of agriculture in Africa depends on one thing above all:

connection.

Learn more and explore collaboration opportunities:

👉 AgriLink Africa Official Website

FAQs on Agricultural Finance Africa

1. Why is agricultural finance Africa so limited?

Agricultural finance Africa is limited due to high risks, lack of reliable data, fragmented value chains, and weak infrastructure, making it difficult for banks to assess and manage lending.

2. What makes agriculture “unbankable” in Africa?

Agriculture becomes unbankable when there is no data, no integration, and high uncertainty in production and markets—key challenges in agricultural finance Africa.

3. How can agricultural finance Africa be improved?

Agricultural finance Africa can be improved by building data systems, digitizing value chains, strengthening cooperatives, and introducing risk-sharing mechanisms like insurance and guarantees.

Abenezer Wondimagegn is the Founder & CEO of AgriLink Africa, a Research & Data Analyst, and Article Publisher. He specializes in Agriculture, Supply Chain, Logistics, Nutrition, E-commerce, and Business Investment. Through his work, he empowers farmers, strengthens food systems, and shares insights to drive innovation and sustainable growth in Ethiopia’s agricultural sector.